Obstacles to transformation in the electricity sector

The success of technological innovation projects does not just rely on the development of new technologies. Successful implementation of new technological systems such as the ebalance-plus energy balancing platform requires transformation in multiple dimensions. We identified a broad range of obstacles that flexibility solutions currently face in the European electrical power sector.

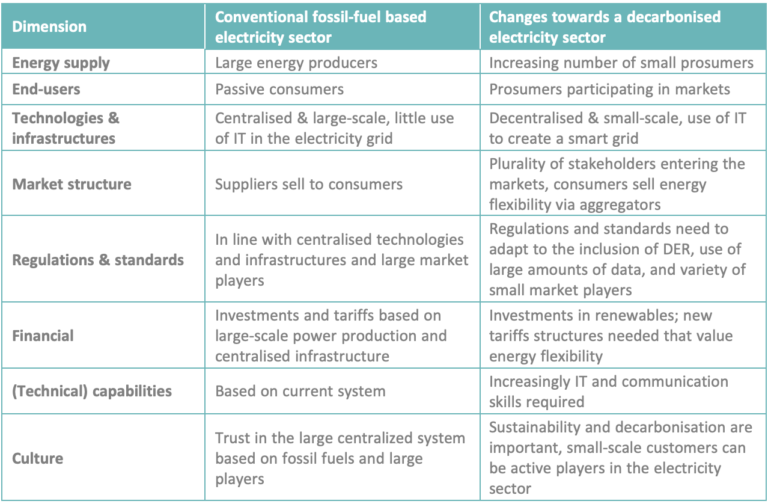

Ebalance-plus is part of a larger transition process that is currently taking place: the decarbonisation of the electricity sector. Changes needed in the electricity sector are inherently “socio-technical”: technological innovation must go hand-in-hand with necessary “social” transformation processes in regulatory frameworks, consumer behaviour, culture, financial structures, capabilities, business models, and markets (see Table below).

For example, the change from large-scale centralised power plants to decentralised technologies based on renewable energy asks for new skills and capabilities of installers and maintenance technicians.

Next, the electricity market needs to be restructured, as more and more smaller players such as aggregators will enter the market and sell energy flexibility of households.

This in turn asks for changes of regulatory frameworks at European and Member State level that have so far regulated big energy suppliers as main market players.

Finally, cultural and behaviour changes from end-users are also necessary, as they need to change from passive consumers to actively responding to dynamic electricity tariffs to help balancing the grid.

As changes in all these dimensions is a complex and contested process that takes many years, technological innovations such as those developed in ebalance-plus, might face many obstacles in their implementation that are not just technical.

Within the ebalance-plus project, several activities ensure that the project partners take these barriers into account in the development of the solutions. First, IPI researched end-user behaviour and developed propositions to motivate users engage with the ebalance-plus flexibility solutions. Second, barriers for the optimal deployment and operation of business models based on the project solutions are analysed as well.

The preliminary results can be categorised into three overarching themes:

- communication and data

- energy flexibility assets

- the market.

Successful implementation of new technological systems requires transformation in many dimensions. As these changes is a complex process that takes many years, technological innovations might face many obstacles in their implementation that are not just technical.

Below we provide a selection of the identified potential obstacles for the projects’ innovations in the electricity sector throughout the EU:

Communication and data-related obstacles:

- The lack of standardisation of systems, protocols and devises complicate interoperability.

- The absence of connectivity of appliances and the low smart readiness of buildings.

- A low smart meter penetration in certain Member States and smart meters that lack functionalities such as time and spatial resolution and remote management.

- Third parties, such as aggregators, have no timely access to smart meter (customer) data in all countries.

- Aggregators and Distribution System Operators (DSOs) are limited in what may be done with customer data because of GDPR.

Energy flexibility assets related obstacles:

- Energy storage assets face many barriers to participate in demand response and electricity markets. Many countries have double grid tariffs or taxes on energy storage.

- Distributed Energy Resources (DER) may not participate in all markets to contribute to voltage control and congestion management. DSOs encounter challenges in deploying DER flexibility to balance the grid.

- A lack of adequate regulations and standards related to Vehicle-to-Grid (V2G) exists in many countries, for example double taxation for bidirectional charging. Charging stations with V2G capabilities are not widespread.

Market structure and mechanisms forming barriers:

- Demand response and aggregated load are not accepted as resources in all markets in Europe, and in markets that are open many access barriers exist.

- DSOs are slow in deploying flexibility for grid management and local flexibility markets are missing. DSOs lack financial incentives to purchase flexibility and are not renumerated to develop new necessary capabilities and skills needed to use flexibility.

- Net-metering and feed-in-tariffs discourage the use of flexibility in certain Member States. Fixed electricity prices in some Member States do not value energy flexibility, dynamic electricity prices are important to unlock end-user’s flexibility.

In the next phase we will analyse the obstacles in specific countries (Denmark, France, Italy, and Spain). These results will be considered in the development of exploitation plans of the project.

By Mara van Welie from ESCI.